Energy firm competition and profit dynamics

While there is an increase in profits from the energy infrastructure in Canada, it is from running the system harder, increased efficiency of output, a little from financial hedging wins, and some from hedging with the physical assets of the fully integrated companies. The profits are high without the effect of price and the price increase has had little impact on that profit growth. This is because the strategy of companies in Canada is cost/asset/capital discipline. Instead of investing in new infrastructure or even maintenance, it is about squeezing the assets and the workers they have for every penny of profits to return to shareholders.

Prices, hedging, and profits

Introduction

With inflation picking-up again because of the global energy crisis, it is important to ask how prices are set, what controls those prices, and if there are things that could mitigate those price increases?

During the pandemic-response, there were price increases most people had not experienced in the West for several decades. At the time, we dived into these discussions, explaining inflation from the more classical perspective and showed how that analysis differed from the orthodox "explanations" such as the mythical "wage-price spirals".

The current crisis is a bit different. Prices are rising for people because of energy and related input cost increases. The focus is mostly around oil, because of the war, but there are also price increases for other energy types and energy-related products like chemicals, renewables, and fuels happening. All these are flowing down the production chain to increase the costs of goods.

Let's take a look at price setting to understand these concepts from a more classical perspective so we can juxtapose those against the popular narratives. Specifically, we are interested in what we can do to bring those prices down in the face of a global energy crisis.

Price and profit

Modern classical economics synthesized by Anwar Shaikh (Real Economic Theory) shows that there is very little "monopoly pricing" in the real world of capitalism. Their analysis shows firms are not able to drive prices higher just to drive their profits up.

Even extremely large, capital intensive firms have other large firms they compete against for profit and investment. Financialized risk models, shareholder structures that allow very fast shifts in investment, futures markets, and debt markets all facilitate competition in a variety of additional (near invisible to the public) ways when it comes to firm-level profitability and costs of production.

In this real world of economics described by Shaikh, the unit of selection in competition is the firm. Just like the unit of selection in biology (evolution) is the individual. Selection ("winning") happens for a variety of reason, both internal and external, but it is what happens to the firm's production of profits that determines its survival from one day to the next.

The constant, turbulent dynamics of real competition over time means which firm is "winning" will change because of those myriad of internal and external factors.

The resulting emergent property of price setting can be seen in a snapshot of time of a firm having the highest profit rate per unit production. The firm with the best technology and production process and lowest input costs in a market demanding their output.

At this moment this firm is the "Regulating Capital" in that competitive market.

What is it regulating? With the highest profit rate it is regulating the terms of battle with its competitors:

- It can reduce prices (within a range) to attract more customers.

- It can match the highest price to maximize profit on each unit of production to maximize investment from outside speculators.

- It can save money to invest later in new machines.

- It could also run-to-fail and maximize returns in the short-term, cannibalizing future cost, if this is the end of the line for its products.

There are many options, but the Regulating Capital gets to choose (within a range) what it does. However, this moment of choice is fleeting. Once a decision is made, other firms respond and—if they respond correctly—they could become the next regulating capital. And, so on and so forth.

A turbulent dynamic results.

There are implications for price in this real world of turbulence. It is not a simple dynamic of being able to increase prices through "monopoly power", the price is a result of these internal and external factors, real costs, real wages, and real demands by investors working to affect the choices made in firms.

Additionally, this turbulent dynamic and competition also exists along and between different parts of the supply chain of production to make the "final" products sold and used.

The result is that price and profit are not connected directly, nor are either controlled by any one firm at all times. And, it means firms cannot set prices independently from profits and competition pressures.

As discussed before, prices are to inflation as weather is to climate change. The relationship is not necessarily intuitive or obvious.

With this in mind lets have a look at energy prices and profit rates during the current energy crisis.

"Energy prices" are not a single thing. There are many "prices" because there are many types of energy.

Energy comes in many forms and is much less impacted by oil (and natural gas) availability than it used to be, even a decade ago. While the current crisis is about oil, specifically supply of oil being disrupted by trade in physical crude, it affects energy in other forms around the worlds as well.

The reason that the impact is "global" is because crude oil (the source material of all other petroleum inputs and fuels) is only extracted in large quantities in a few countries but is necessary in all countries.

If a country is an oil exporter or importer, you are part of this global system of distribution. A country cannot escape these global dynamics, or the prices, unless it can cut itself off from the world completely. This is not possible over a short period of time.

And, it is not just energy product that needs to be cut off because the simple action of not selling into a market will invite responses from firms and other countries attempting to also deal with the crisis. These are dynamics that cannot be avoided or mitigated over the medium term.

Especially when that country might sit beside the American Empire.

Prices and hedges

Producers of basic commodities have used hedging strategies for as long as they have faced bad weather, natural disasters, war, and other infrequent catastrophes.

Producers of wheat, rice, and pulses have dried and stored (in a bank) a portion of crops in good growth years to hedge against less good years.

Oil and mining producers are no different. The cost of transport and other uncontrollable things that cause changes to price need a hedge. The alternative is years of blowout profits followed by years of bankruptcy. States and private "banks" have played a role of this through history well before capitalism.

Modern capitalism has birthed a financialized system for hedging on price and the time it takes to grow, mine, refine, transport, and transform products from procurement to taking possession.

These hedging strategies, be they putting product aside to buying insurance/hedge on price fluctuations, save firms from bankrupcy when prices collapse. But, through the same mechanism dampen profits from large price increases.

There are ways these firms who produce try to play in the financial market, by settings trading floors. But just because a firm specializes in a product does not mean it has any particular special knowledge in financial markets. If it does have specific knowledge of where they market it, it would engage in physical hedging (changing production volumes, storage, and transport speed), negating need for "hedging the hedge" financially.

To add to the complexity, companies like BP (and Total) are different kind of "oil companies" compared to smaller firms like those in Canada. While most smaller oil companies has a trading desk to do hedging against price fluctuations, BP is more of a financial bank than it is an oil company and it is the firm that smaller firms buy their hedge from.

BP turned into a financial bank and trading desk for paper oil in the 70s. It made large amounts of money from the crisis at that time, but its assets were nationalized in the Middle East. In response, it put its new windfall profits into starting a trading desk to make money on selling a hedge position to the newly established nationalized oil companies.

While BP and Shell are substantially bigger than Suncor and CNQ (at least three to four times). Also, you can see how these companies are structured showing they are vastly different:

- Canadian Natural Resource Limited (CNQ) is nearly 95% physical asset.

- Suncor is three quarters a physical asset company.

- BP is less than one third a physical asset company, the rest is financial.

- Shell is less than fifty per cent physical.

- Trafigura, a specialized financial oil investment firm is 5% physical.

BP makes way more profit when hedges against price volatility it sells to other oil companies work in its favour than it does from physical oil (which it still makes money from. The current crisis of unexpected increased prices are exactly this situation.

Suncor is more financialized than CNQ because it hedges across a wider variety of physical assets because of its integration from producer to refiner to pipelines to retail.

In fact, what we call Oil Majors are not really the same kind of companies at all.

- BP is a major paper oil trading firm.

- Shell is a natural gas futures trading firm.

- Total is an electricity market hedging firm.

From the Real Economics Theory frame, it is also interesting to look at the profit rates of each type of company. Suncor and Shell are very similar in profit rates on their physical assets, showing a comparable efficiency of production, but Suncor is tiny on paper oil in financial markets.

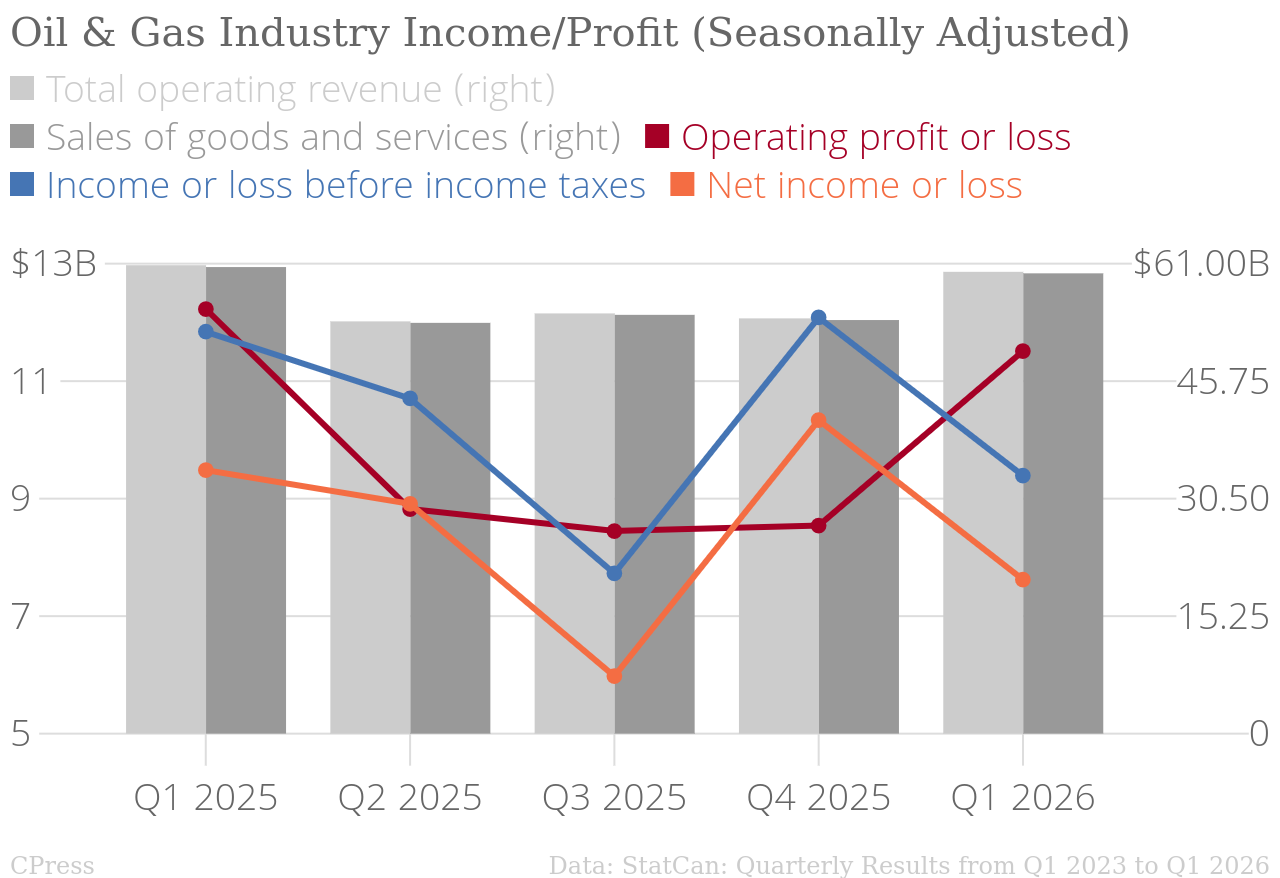

Profits

There are large profits made by Canadian oil firms, but they are not from price increases. The profits are from increasingly efficient extraction, increased output (by expanding oil export market options).

The top six firms in Canada are Enbridge, Suncor, Imperial Oil, CNQ, Cenovus, and TC Energy. Two of those are pipeline companies making a significant amount of their profits in the USA. But, for the sake of argument, we will include them here.

Total proifts in the first quarter of 2026 is $9.69B. This compares to $7.90B for the fourth quarter of 2025. A near 23% increase.

$6.9B was sent to shareholders.

While there is an increase in profits from the energy infrastructure in Canada, it is from running the system harder, increased efficiency of output, a little from financial hedging wins, and some from hedging with the physical assets of the fully integrated companies.

The profits are high without the effect of price and the price increase has had little impact on that profit growth. This is because the strategy of companies in Canada is cost/asset/capital discipline. Instead of investing in new infrastructure or even maintenance, it is about squeezing the assets and the workers they have for every penny of profits to return to shareholders.

A deeper dive into volatility, pricing of crude, and profits

Background

Turbulent regulation:

It is expected that the arbitrage and hedging process companies use to maximize their profits results in constant fluctuations of paper oil prices over time (and, over longer-terms, physical oil prices). Oil is a physical thing and takes time to move. It is this time that is essential in determining local revenue and profits for different parts of the energy market.

None of the profits of different parts of the energy market move in unison.

Here are some examples of the different parts of the energy market we are interested in following from this perspective:

- Physical prices: the price to buy actual oil.

- Paper prices: the price of financial derivatives for oil (futures) trading on an exchange based on a guess what the future price might be.

- (Terminal) Rack Prices: wholesale price of product of refining (gasoline and diesel varieties).

- Hedging: using financialization (derivatives) through trading the paper price of crude to protect against swings in the real price of oil during its travel (along pipelines and in trains/ships/trucks) from production to refining to product (weeks) or in swings in Crack Spread.

- Inventory hedging: shifting speed of movement or storage of physical oil assets in response to price shifts.

- Volatility: the size of the price swings over time.

- Crack Spread: Shifting price difference between a barrel of crude and resulting product (gasoline) from that barrel.

- Arbitrage: the process of deciding where to produce/sell/transport the product or the financialized paper contract in search of profit maximizing.

Trading platforms:

- NYMEX (New York Mercantile Exchange): West Texas Intermediate (WTI) futures and gasoline (RBOB) price-setting exchanges.

- ICE (Intercontinental Exchange): Brent Crude (oil's global benchmark) and Gasoil exchange.

- ICE NGX: Canada's Western Canadian Select (WCS) oil and natural gas exchange.

Analysis

Financial hedging for most oil companies is about protecting margins on physical oil, not driving profits. There are some exceptions to this (see note above about BP).

There is no monopoly on price setting, so hedging is necessary for firms to protect their margins in the face of price volatility.

As prices go up for physical oil, there is a profit gain for producers, but hedging takes some of that profit. There is a larger potential for a windfall profits when prices come down. Again, determined by speculation, competition, and playing their strength along the supply chain well.

During the current global crude crisis, paper contracts (hedging) for companies realized huge losses, resulting in downward pressure on revenue immediately.

Profits on the increased price for physical oil is not made until later. However, net profits across the year are not guaranteed on this physical product and are dependent on many additional factors.

- Financial investment firms that thought the disruption to supply would be short-lived have lost significant money in margin calls on their hedges. When shifts in price did not arrive the difference was extremely large, meaning commodity traders (including some oil companies like Suncor) had to spend a lot of money covering those losses resulting in sales of other (financial) assets.

-

In a price drop scenario, physical product is going to stay expensive in the short-term because of physical supply lagging the future price that sets paper prices. Paper margins could also grow, but physical oil will be high cost for refineries.

- Temporary profit bump for dealing with physical oil at retail centres.

- Profits should increase on both physical and paper profits for oil majors.

- During fast price drops, upstream paper profits depend entirely on hedging strategy. If companies are sufficiently "short" the price (guess correctly when prices fall) then they gain by capturing the falling price. If they are "long" then they will lose money on each barrel compared to competitors (including commodity trading firms).

For Suncor and other integrated companies, any suggestion of "windfall" profits depend on hedging strategies and rate of fall of the oil price.

Type of petroleum energy companies in Canada

There are different types of energy companies in Canada and each experience changes in the market price volatility differently.

- Fully integrated (Suncor)

- Mostly integrated (Imperial minus retail)

- Refinery owners (Tidewater, Co-op in Regina)

- Retail mostly (Sunoco/Parkland)

- Pure play extraction (CNQ)

The addition complications to the profit analysis are:

- Canadian companies exporting to refineries in USA are limited by pipeline and rail capacity, but also demand limited by refining capacity in the USA.

- Export to Asia is limited by capacity through TMX, rail capacity, port congestion, and who globally is willing to buy the oil (at that price) when it hits a boat.

- Local refining capacity and price differential between local refining and export.

- Import from American pipelines of crude or refined product.

- USD/CAD exchange rate. Weak CAD acts to increase profits for producers in Canada, but pressure on refineries who import.

The final issue putting downward pressure on profits is that Canadian super heavy sour crude can only be refined in specialized refineries around the world. Outside of North America, capacity to refine WCS exist in a few places in advanced China refineries and India with some very small volumes taken by others. Even at the refineries in China that will take WCS, it is for mixing with other varieties of crude and it is competing on price and access with other types. These Chinese refineries are set-up to take a variety of types, switching based on price.